On Tue, 29 Jul 2025 12:01:04 -0400, Tom Elam wrote :

Why do Apple owners buy their phones twice by paying for this garbage?

Samsung offers almost the same plan for their phones and tablets. Why do

Samsung owners buy this plan?

That's a good question that I do not know the answer for so what I'll do is ask that question on the Android newsgroup to see if anyone is buying it.

I doubt many Android owners would fall for the insurance plan trick though.

Insurance is for things you can't replace, where a phone is something you

can easily replace so it would be absurd for Samsung owners to buy it.

I own a Samsung. I got it for free. Actually I paid $18 tax and then I

added a $9 case plus a $3 screen plus a $20 sd card to multiply storage.

Hence, my Samsung Galaxy A32-5G cost me about $50 in April of 2021.

Standard AppleCare+ = $10.49/month = $1,258.80 for an iPhone 16.

AppleCare+ with Theft and Loss = $11.99 /month = $1,438.80/10 years

You're paying just for insurance, 26 times what my phone costs.

I doubt seriously that your phone was free.

How do you know anything about how many Apple devices have AppleCare?

Cars are easily replaced. Expensive, but not a problem finding a car. By your logic you should not insure your car.

On Tue, 5 Aug 2025 13:05:37 -0400, Tom Elam wrote :

I doubt seriously that your phone was free.

We discussed this on this very newsgroup in April or May of 2021 and a

bunch of people on this very newsgroup took advantage of the deal.

How do you know anything about how many Apple devices have AppleCare?

I don't think I said how many people buy this crappy insurance, as I

wouldn't know why anyone would buy insurance on a commodity like a phone.

Cars are easily replaced. Expensive, but not a problem finding a car. By

your logic you should not insure your car.

I don't even insure my house, Tom, because it's paid for and I can replace

it if I ever need to. So why would I insure my 30-year old automobiles?

I only insure liability. Not damage or replacement which I can pay for. Insurance is never a good deal unless you can't replace what is lost.

"Apple has effectively turned extended warranties and insurance intoa subscription product, with an ongoing monthly or annual payment."

On 2025-08-06 15:22, Marion wrote:

On Tue, 5 Aug 2025 13:05:37 -0400, Tom Elam wrote :

I doubt seriously that your phone was free.

We discussed this on this very newsgroup in April or May of 2021 and a

bunch of people on this very newsgroup took advantage of the deal.

The "deal" doesn't make the phone free.

It just means you're paying for a pretty basic phone month-by-month.

How do you know anything about how many Apple devices have AppleCare?

I don't think I said how many people buy this crappy insurance, as I

wouldn't know why anyone would buy insurance on a commodity like a phone.

Every choice to buy insurance is a gamble.

Cars are easily replaced. Expensive, but not a problem finding a car. By >>> your logic you should not insure your car.

I don't even insure my house, Tom, because it's paid for and I can

replace

it if I ever need to. So why would I insure my 30-year old automobiles?

Riiiiiiiight.

I only insure liability. Not damage or replacement which I can pay for.

Insurance is never a good deal unless you can't replace what is lost.

Every choice to buy insurance is a gamble.

Precisely, and from a business model standpoint, the insurance costs

have to exceed the expected average cost of claims, plus overhead, in

order for the insurance company to remain fiscally viable. This means

that it is always statistically against the customer, yet they often

elect to buy insurance anyway, for a variety of reasons.

Cars are easily replaced. Expensive, but not a problem finding a

car. By

your logic you should not insure your car.

I don't even insure my house, Tom, because it's paid for and I can

replace

it if I ever need to. So why would I insure my 30-year old automobiles?

Riiiiiiiight.

Well, he does have one valid point here: the cost of collision

insurance on their 30 year old clunker isn't a good value.

I only insure liability. Not damage or replacement which I can pay for.

Insurance is never a good deal unless you can't replace what is lost.

Its not merely if one can afford to. One needs adequate liquidity in

order to self-insure, as well as the willingness to self-insure.

I doubt seriously that your phone was free.

On 8/7/2025 4:02 PM, -hh wrote:Perhaps Marion is admitting that they live in Florida and can't afford

Alan wrote:

[Marion wrote]:

...

I don't even insure my house, Tom, because it's paid for and I can

replace it if I ever need to. So why would I insure my 30-year old

automobiles?

You should not normally carry collision or comprehensive on a 30 year. However, if it has market value as a collectable you might find it worthwhile. Liability is required by law in many states.

Homeowner insurance is justified based on premium relative to market

value. High risk areas - Florida coastline - with high premiums per

$1000 value versus my case with a $500,000 home with a $1,181 annual

premium for home, contents and liability is a no-brainer. I insure it.

As they've not already said "Hemmings" ... hypotheticals need not apply.What if it is a low mileage 1965 Mustang in mint condition.Riiiiiiiight.

Well, he does have one valid point here: the cost of collision

insurance on their 30 year old clunker isn't a good value.

I only insure liability. Not damage or replacement which I can pay for. >>>> Insurance is never a good deal unless you can't replace what is lost.

I hate to admit it but I have had enough auto claims to make it

worthwhile to insure my car.

Its not merely if one can afford to. One needs adequate liquidity in

order to self-insure, as well as the willingness to self-insure.

Yep. I never had an umbrella policy, even though I ran a business.

On 8/7/2025 4:02 PM, -hh wrote:

Every choice to buy insurance is a gamble.

Precisely, and from a business model standpoint, the insurance costs

have to exceed the expected average cost of claims, plus overhead, in

order for the insurance company to remain fiscally viable.� This means

that it is always statistically against the customer, yet they often

elect to buy insurance anyway, for a variety of reasons.

True. You are betting that statistically small but expensive event will exceed the premiums.

Cars are easily replaced. Expensive, but not a problem finding a car. By >>>>> your logic you should not insure your car.

I don't even insure my house, Tom, because it's paid for and I can

replace it if I ever need to. So why would I insure my 30-year old

automobiles?

You should not normally carry collision or comprehensive on a 30 year. However, if it has market value as a collectable you might find it worthwhile. Liability is required by law in many states.

I doubt seriously that your phone was free.

We discussed this on this very newsgroup in April or May of 2021 and a

bunch of people on this very newsgroup took advantage of the deal.

The "deal" doesn't make the phone free.

It just means you're paying for a pretty basic phone month-by-month.

Which has already been explained to him.

Every choice to buy insurance is a gamble.How do you know anything about how many Apple devices have AppleCare?

I don't think I said how many people buy this crappy insurance, as I

wouldn't know why anyone would buy insurance on a commodity like a phone. >>

Precisely, and from a business model standpoint, the insurance costs

have to exceed the expected average cost of claims, plus overhead, in

order for the insurance company to remain fiscally viable. This means

that it is always statistically against the customer, yet they often

elect to buy insurance anyway, for a variety of reasons.

Cars are easily replaced. Expensive, but not a problem finding a car. By >>>> your logic you should not insure your car.

I don't even insure my house, Tom, because it's paid for and I can

replace

it if I ever need to. So why would I insure my 30-year old automobiles?

Riiiiiiiight.

Well, he does have one valid point here: the cost of collision

insurance on their 30 year old clunker isn't a good value.

I only insure liability. Not damage or replacement which I can pay for.

Insurance is never a good deal unless you can't replace what is lost.

Its not merely if one can afford to. One needs adequate liquidity in

order to self-insure, as well as the willingness to self-insure.

True. You are betting that statistically small but expensive event will exceed the premiums.Every choice to buy insurance is a gamble.

Precisely, and from a business model standpoint, the insurance costs

have to exceed the expected average cost of claims, plus overhead, in

order for the insurance company to remain fiscally viable.� This means

that it is always statistically against the customer, yet they often

elect to buy insurance anyway, for a variety of reasons.

Cars are easily replaced. Expensive, but not a problem finding a

car. By

your logic you should not insure your car.

I don't even insure my house, Tom, because it's paid for and I can

replace

it if I ever need to. So why would I insure my 30-year old automobiles?

You should not normally carry collision or comprehensive on a 30 year. However, if it has market value as a collectable you might find it worthwhile. Liability is required by law in many states.

Homeowner insurance is justified based on premium relative to market

value. High risk areas - Florida coastline - with high premiums per

$1000 value versus my case with a $500,000 home with a $1,181 annual

premium for home, contents and liability is a no-brainer. I insure it.

What if it is a low mileage 1965 Mustang in mint condition.Riiiiiiiight.

Well, he does have one valid point here:� the cost of collision

insurance on their 30 year old clunker isn't a good value.

I only insure liability. Not damage or replacement which I can pay for. >>>> Insurance is never a good deal unless you can't replace what is lost.

I hate to admit it but I have had enough auto claims to make it

worthwhile to insure my car.

Its not merely if one can afford to.� One needs adequate liquidity in

order to self-insure, as well as the willingness to self-insure.

Yep. I never had an umbrella policy, even though I ran a business.

Homeowner insurance is justified based on premium relative to marketPerhaps Marion is admitting that they live in Florida and can't afford

value. High risk areas - Florida coastline - with high premiums per

$1000 value versus my case with a $500,000 home with a $1,181 annual

premium for home, contents and liability is a no-brainer. I insure it.

P&C (&/or its so run down that its uninsurable).

I've seen both happen, as Florida's P&C (not even for "coastline")

cracked 2% back in 2023 and is roughly 2.3% today. For a $500K home,

that's over $11K/year just for P&C with no extra frills.

I hate to admit it but I have had enough auto claims to make it

worthwhile to insure my car.

Claims vs age tend to follow a "bathtub" curve.

Its not merely if one can afford to.� One needs adequate liquidity in

order to self-insure, as well as the willingness to self-insure.

Yep. I never had an umbrella policy, even though I ran a business.

Umbrellas are another tool too; never ran an enterprise without one;

figure ~.05%

I doubt seriously that your phone was free.

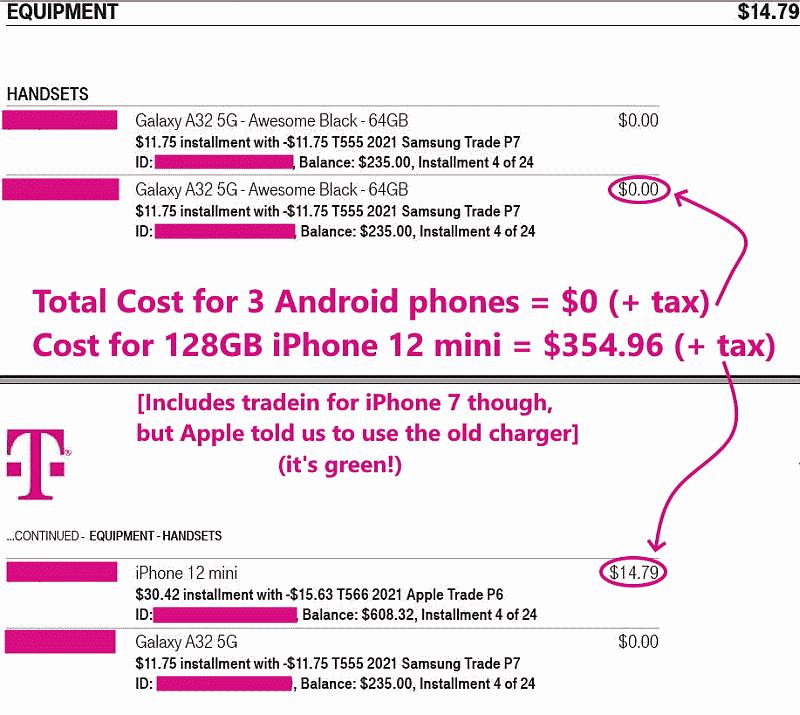

I suspect that it was "free" in the sense that there was no upfront

cost. Typically, for mid-range phones like that it's "$0.00/month for 24 months with promotion." Now it's the A36 5G, a few years ago it was the

A32 5G.

Of course, as we all know, the cost of the phone is simply built into

the monthly fees.

I.e.:

"Recurring promotional savings: $399.99

Credit of $16.67 over 24 months

If you cancel before 24 credits, credits stop and balance on required finance agreement may be due; contact us. For well-qualified customers,

plus tax."

The cheapest plan is $50 per month.

I can buy that phone, unlocked, for about $380, paying about $15.83 per month, and then sign up for a prepaid plan for a lot less.

Or I can buy it for about $200, locked for 60 days, buying two months of

the least expensive plan from a Verizon MNO.

If you're sticking with a carrier that offers monthly credits on phone purchases then it makes sense to take advantage of these offers since they're not giving you some other discount if you choose not to take the "free" phone.

People that are bad at math think that they're getting a "free" phone.

On Thu, 7 Aug 2025 22:55:42 -0400, -hh wrote :

Homeowner insurance is justified based on premium relative to marketPerhaps Marion is admitting that they live in Florida and can't afford

value. High risk areas - Florida coastline - with high premiums per

$1000 value versus my case with a $500,000 home with a $1,181 annual

premium for home, contents and liability is a no-brainer. I insure it.

P&C (&/or its so run down that its uninsurable).

Ummm.. I've been on this ng for, oh, I don't know, almost as long as it has existed, & I've *always* said I lived in the Santa Cruz mountains.

Everyone who is here knows that. So if you do not know it, why not?

I've seen both happen, as Florida's P&C (not even for "coastline")

cracked 2% back in 2023 and is roughly 2.3% today. For a $500K home,

that's over $11K/year just for P&C with no extra frills.

This reference says premiums are $5,000 to $12,000/year per 300K of value.

<https://getsafeandsound.com/blog/average-fire-insurance-cost-california/>

Trust me, no home is less than a million and most are multiple millions.

Add it up.

...

My car is 30 years old. According to the insurance company and the local

car auction business, it is worth somewhere between NZ$3000 and

NZ$5000 ... but the greedy idiots on the local eBay clone website, are putting starting prices of about ten times that amount, between

NZ$30,000 and NZ$40,000 (I haven't bothered tracking the sales, but I

doubt any of them actually get bought).

On 8/8/25 06:37, Marion wrote:

On Thu, 7 Aug 2025 22:55:42 -0400, -hh wrote :

Homeowner insurance is justified based on premium relative to marketPerhaps Marion is admitting that they live in Florida and can't afford

value. High risk areas - Florida coastline - with high premiums per

$1000 value versus my case with a $500,000 home with a $1,181 annual

premium for home, contents and liability is a no-brainer. I insure it.

P&C (&/or its so run down that its uninsurable).

Ummm.. I've been on this ng for, oh, I don't know, almost as long as

it has

existed, & I've *always* said I lived in the Santa Cruz mountains.

Which "this ng"? This is being cross-posted between CSMA and MPMI.

Everyone who is here knows that. So if you do not know it, why not?

Possibilities include:

a) different "this ng";

b) you've not been an important enough contributor to pay attention to;

c) A & B.

I've seen both happen, as Florida's P&C (not even for "coastline")

cracked 2% back in 2023 and is roughly 2.3% today. For a $500K home,

that's over $11K/year just for P&C with no extra frills.

This reference says premiums are $5,000 to $12,000/year per 300K of

value.

<https://getsafeandsound.com/blog/average-fire-insurance-cost-

california/>

$5K/$300K = 1.7% and $12K/$300K = 4%, so the basic observation applies: homeowners who can't afford P&C (&/or the property is uninsurable).

For FL, the rate of uninsured homeowners is estimated at 15%-20%, with

the latter being the newest estimates; roughly 2x that of CA>

Oh, no!Trust me, no home is less than a million and most are multiple millions.

Add it up.

How about a 3BR/2BA with a $59K asking price *and* in Santa Cruz, CA?

Its at 2395 Delaware Ave, #126

Here's the listing; it looks to be just ~400m from the water:

<https://www.zillow.com/homedetails/2395-Delaware-Ave-126-Santa-Cruz- CA-95060/453069643_zpid/>

...

Maybe I'm stupid & you trolls are smarter than I (i.e., Alan Baker, Jolly Roger, Tom Elam, -hh & Your Name) - which - if true - you can prove it.

...Every choice to buy insurance is a gamble.

Precisely, and from a business model standpoint, the insurance costs

have to exceed the expected average cost of claims, plus overhead, in

order for the insurance company to remain fiscally viable. This means

that it is always statistically against the customer, yet they often

elect to buy insurance anyway, for a variety of reasons.

Which means, on average, the customer loses.

Unless they know something the insurance company doesn't know.

Because then (and only then) the insurance company calculations would be overly optimistic in terms of how much money the insurance company makes.

But if you tell the truth on insurance applications & claims, then, on average, you will always pay more for insurance than for the losses.

Hence, it's a logical psychological conclusion that you probably should consider only paying insurance on things you can't very easily replace.

Except that paying cash isn't really a factor which determines ifWell, he does have one valid point here: the cost of collision

insurance on their 30 year old clunker isn't a good value.

All my vehicles are old because I maintain them myself, and, since I paid cash for them at the time I bought them new, I didn't need collision.

I've written tutorials on how to mount and balance tires at home...Irrelevant, although that does reinforce that your opinion is quite

But to insure a car that isn't worth the money for insurance is folly.

I own multiple homes ...With or without counting the garden shed in back? /s

Of course, if I moved into one of them, I'd lose the rent, but my mainNone of which has anything to do with insurance, so its not clear why

point you seem to understand, which is that insurance is a calculation.

All you get out of insurance is being able to fix/replace something thatNo, that's not the only thing that one gets out of insurance, since one

you wouldn't otherwise be able to fix/replace it - which is valuable.

But not for a phone.Maybe, maybe not: depends on one's free cash flow, as well as otherpersonal factors, including time.

On 8/8/25 02:32, Your Name wrote:

...

My car is 30 years old. According to the insurance company and the

local car auction business, it is worth somewhere between NZ$3000 and

NZ$5000 ... but the greedy idiots on the local eBay clone website, are

putting starting prices of about ten times that amount, between

NZ$30,000 and NZ$40,000 (I haven't bothered tracking the sales, but I

doubt any of them actually get bought).

If I did the currency conversion correctly, that's like roughly US$3000.

Locally (US East Coast), the proverbial "anything which still runs" is easily worth that much.

For example, a neighbor just dropped US$15K last month for a 15 year

old compact Japanese SUV (Sorry, I forget which make/model).

Pre-CoVid, I would've considered that to be nearly ~twice what it was probably worth. But the markets have changed...supply & demand and

all that bit.

-hh

Hence, it's a logical psychological conclusion that you probably should

consider only paying insurance on things you can't very easily replace.

Incorrect, as has already been explained: there's more factors under consideration than merely if one can afford it or not. Another example

is one of personal convenience & time savings. If you've ever had an accident with a rental car while not paying for the carrier's insurance, you'd have a better insight on these ramifications.

Except that paying cash isn't really a factor which determines ifWell, he does have one valid point here: the cost of collision

insurance on their 30 year old clunker isn't a good value.

All my vehicles are old because I maintain them myself, and, since I paid

cash for them at the time I bought them new, I didn't need collision.

insurance is required: it is the party who holds the title who decides.

Car loans commonly require having collision & comprehensive: they're the party who's primarily incurring the risk of loss, so its their decision

they make as a condition of the loan. Don't like that? Go elsewhere.

I've written tutorials on how to mount and balance tires at home...Irrelevant, although that does reinforce that your opinion is quite

likely being biased by your financial situation & ability to afford.

But to insure a car that isn't worth the money for insurance is folly.

Hence, your's ain't no collectable(s). As you posted separately:

My vehicles are a bimmer and a few Toyotas, none of which are

collectibles. The bimmer is always broken but the Toyota's last forever.

If your BMW is broken down all the time, blame its mechanic. Ditto for

the rest of the hulks resting on cinder blocks in the yard.

I own multiple homes ...With or without counting the garden shed in back? /s

Of course, if I moved into one of them, I'd lose the rent, but my mainNone of which has anything to do with insurance, so its not clear why

point you seem to understand, which is that insurance is a calculation.

this aside was mentioned. Copying Tommy's brag attempts?

All you get out of insurance is being able to fix/replace something thatNo, that's not the only thing that one gets out of insurance, since one

you wouldn't otherwise be able to fix/replace it - which is valuable.

can insure for more than one's present net worth: a classic example of

that is of life insurance, especially of term life when young.

But not for a phone.Maybe, maybe not: depends on one's free cash flow, as well as otherpersonal factors, including time.

On Fri, 8 Aug 2025 16:00:02 -0400, -hh wrote :

Hence, it's a logical psychological conclusion that you probably should

consider only paying insurance on things you can't very easily replace.

Incorrect, as has already been explained: there's more factors under

consideration than merely if one can afford it or not. Another example...

So -hh is correct...

Car loans commonly require having collision & comprehensive: they're the

party who's primarily incurring the risk of loss, so its their decision

they make as a condition of the loan. Don't like that? Go elsewhere.

Not only car loans. House loans too. They all require insurance coverage. Only if you own the title do you get to choose what kind of coverage.

I've written tutorials on how to mount and balance tires at home...Irrelevant, although that does reinforce that your opinion is quite

likely being biased by your financial situation & ability to afford.

I've mounted my own tires my whole life, but I've been retired for about 20 years, so there's not a lot of income but that doesn't matter for this.

My point is some people are self sufficient; some are not.

up choosing other products instead.But to insure a car that isn't worth the money for insurance is folly.

Hence, your's ain't no collectable(s). As you posted separately:

My vehicles are a bimmer and a few Toyotas, none of which are

collectibles. The bimmer is always broken but the Toyota's last forever.

If your BMW is broken down all the time, blame its mechanic. Ditto for

the rest of the hulks resting on cinder blocks in the yard.

Well, it's clear you've never owned a bimmer or beemer or Toyota then.They've made the short list and I've taken test drives, but have ended

I was making a point about design styles - which are hugely different.

I own multiple homes ...

With or without counting the garden shed in back? /s

I'm not sure why you feel you need to insult, but insult away.

I've been on Usenet for decades - I don't think you'll make me leave.Ah, its the old "decades" brag attempt. Was that because you had AOL?

event is *your* personal failure to have adequate risk diversification.Of course, if I moved into one of them, I'd lose the rent, but my main

point you seem to understand, which is that insurance is a calculation.

None of which has anything to do with insurance, so its not clear why

this aside was mentioned. Copying Tommy's brag attempts?

My point was about catastrophic losses that encompass wide areas.

Didn't you understand it?Yup: your clustering of your real estate to be vulnerable to a singular

It's one of the most important considerations any insurance has.

If you don't understand that concept, you may need to learn a lot more.

All you get out of insurance is being able to fix/replace something that >>> you wouldn't otherwise be able to fix/replace it - which is valuable.

No, that's not the only thing that one gets out of insurance, since one

can insure for more than one's present net worth: a classic example of

that is of life insurance, especially of term life when young.

Well, this is true, but I'm an octogenarian, so I don't know what they'll charge for life insurance, but I'm not planning on getting it anytime soon.

Still, I agree that some things like life insurance are valued at manyIts not really your place to try to claim who is "normal" or not.

times what the current earnings of a person are - but they are valued at

the approximation of the total earnings of that person over his lifetime.

Hence, yet again, the calculation is against you unless you happen to know something that the insurance company doesn't know (like if you smoke).

But not for a phone.personal factors, including time.

Maybe, maybe not: depends on one's free cash flow, as well as other

Well, the whole point is that people who buy the extended warranty on a

phone are quite a different kind of person than a normal person is.

Of course there's nothing wrong with DIYing as much as one reasonably

wants to, so long as it is what one actually wants to do, as opposed to needing to do so due to constrained options, especially when one can't

admit said constraint as one's true underlying motivator.

I was making a point about design styles - which are hugely different.

Not successfully, for you compared their reliability, not style.

Well, the whole point is that people who buy the extended warranty on aIts not really your place to try to claim who is "normal" or not.

phone are quite a different kind of person than a normal person is.

On Sat, 9 Aug 2025 14:56:01 -0400, -hh wrote :

Of course there's nothing wrong with DIYing as much as one reasonably

wants to, so long as it is what one actually wants to do, as opposed to

needing to do so due to constrained options, especially when one can't

admit said constraint as one's true underlying motivator.

In general, there are a few people who understand complicated things, and there are even more people who do not understand complicated things.

Those who understand things, can DIY.

Those who do not understand things, cannot DIY.

The operative word there is "can", since I do agree with you that "can" and "want to" are two different things (as is "having to" do it).

1. Some people are intelligent, so they "can" DIY complicated things.

2. Most people are incredibly stupid, so they "can't" handle complexity.

3. Still others, can handle it, but don't want to handle it.

4. And yet others can't afford to have someone else do the work.

My whole life I did my own work as I've never been to a mechanic.

Even when I was 18, I worked on my own cars and bikes.

Hell, when I was 10 or 15 or so, I fixed my own bicycles too.

I've always been someone who can DIY.

But most people aren't intelligent enough to understand complicated things. Those people can not DIY. It's a function of capabilities.

Just like it is with insurance, in a roundabout way.

I can afford to not have insurance; many people can not.

However, my premise is EVERYONE can afford not to have phone insurance.

Since a phone is a cheap commodity.

I was making a point about design styles - which are hugely different.

Not successfully, for you compared their reliability, not style.

Well, I didn't mean "style" as in "stylish" but as in "philosophy".

BMW engineers are atrocious at building the complete system.

But BMW engineers are some of the best in the world in designing suspension systems and drive trains.

Their philosophy is that only the drive train & suspension matters.

The rest they don't care about.

So everything breaks.

Constantly.

Because it sucks.

Compare that to a Toyota.

Big difference.

On Sat, 9 Aug 2025 14:56:01 -0400, -hh wrote :

Of course there's nothing wrong with DIYing as much as one reasonably

wants to, so long as it is what one actually wants to do, as opposed to

needing to do so due to constrained options, especially when one can't

admit said constraint as one's true underlying motivator.

In general, there are a few people who understand complicated things, and there are even more people who do not understand complicated things.

Those who understand things, can DIY.

Those who do not understand things, cannot DIY.

The operative word there is "can", since I do agree with you that "can" and "want to" are two different things (as is "having to" do it).

{more tangential deflection words}

Just like it is with insurance, in a roundabout way.

I can afford to not have insurance; many people can not.

However, my premise is EVERYONE can afford not to have phone insurance.

Since a phone is a cheap commodity.

I was making a point about design styles - which are hugely different.

Not successfully, for you compared their reliability, not style.

Well, I didn't mean "style" as in "stylish" but as in "philosophy".

BMW engineers are atrocious at building the complete system.

But BMW engineers are some of the best in the world in designing suspension systems and drive trains.

Their philosophy is that only the drive train & suspension matters.

The rest they don't care about.>

So everything breaks.

Constantly.

Because it sucks.

Compare that to a Toyota.

Big difference.

Nope, my point was in the portion you "bravely" snipped so as to avoidWell, the whole point is that people who buy the extended warranty on aIts not really your place to try to claim who is "normal" or not.

phone are quite a different kind of person than a normal person is.

Well, anyone who pays for something they definitely do not need to pay for, (like phone insurance) is already making poor decisions. I guess your point is that such stupid people are normal, where the intelligent people are of

a higher order than a normal person (who is incredibly stupid).

https://9to5mac.com/2025/07/25/everything-you-need-to-know-about-applecare-one/

"Apple has effectively turned extended warranties and insurance

into a subscription product, with an ongoing monthly or annual payment."

The plan costs $1,200 over the life of a single iPhone.

Gosh, that's a lot of deflecting words to try to distract from the point

of the reality of financial constraints.

BMW engineers are atrocious at building the complete system.

But BMW engineers are some of the best in the world in designing suspension >> systems and drive trains.

Nope. You're conflating design intent with designer skill or quality.

Compare that to a Toyota.

Big difference.

Because of a different design intent, partly due to Deming.

Another AppleCare+ example. My iPhone 14 was starting to charge

erratically. Wiggling the charging cable left-to-right while it was

plugged in would make it stop charging if you moved it right.

My first cell phone, circa 1998, stopped charging just after it went out

of 1 year warranty. Had to buy another one. Bad experience.

BUT, this time I just took the iPhone over to the local Apple Store, confident that if it was the charging port it could be fixed or even replaced under AppleCare+ terms. It took about 5 minutes to repair. Accumulated lint in the port that the store rep cleaned out. If the

Apple rep had screwed up the port in the process so be it. The peace of

mind knowing I would not be buying another phone is worth the monthly premium to me.

On Sun, 10 Aug 2025 20:45:15 -0400, -hh wrote :

Gosh, that's a lot of deflecting words to try to distract from the point

of the reality of financial constraints.

It's refreshing that -hh actually owns critical thinking skills.

This critical-thinking process is rather uncommon for Apple trolls.

To his point, I said in my *first* response that you insure that which you can't afford to replace. If you're so destitute that you can't even afford

to replace your phone, then maybe it would be worth it to pay twice for

that phone (which is what the warranty costs) not to have to pay to replace it.

BMW engineers are atrocious at building the complete system.

But BMW engineers are some of the best in the world in designing suspension >>> systems and drive trains.

Nope. You're conflating design intent with designer skill or quality.

Again, you own critical thought processes.

While BMW 525i cupholders, seats tilts, Behr expansion tankss, CCV valves & Dormand window regulators are legendary for failing - all in the same way

for everyone, the drivetrain & suspension is also legendary for

performance.

It's not that BMW engineers don't have the skill.Incorrect: you're trying to impose your own criteria after the fact,

They're just not paid to think the whole system through.

They're paid to make only some parts legendary.

So marketing can sell people on *those* components.

BMW is all marketing and very little overall system quality after all.

Sound familiar?For you, since you've already failed at holistic system analysis. /s

Compare that to a Toyota.

Big difference.

Because of a different design intent, partly due to Deming.

Interesting you attribute Toyota Production Systems (aka Lean

Manufacturing) to W. Edwards Deming who Shoichiro Toyoda once said there wasn't a day he didn't think about how Dr. Deming influenced their quality.

At Toyota, every component is engineered for longevity and integration.

BMW prioritizes performance and driving dynamics too often at the expense

of long-term reliability in non-drivetrain systems.

To his point, I said in my *first* response that you insure that which you >> can't afford to replace. If you're so destitute that you can't even afford >> to replace your phone, then maybe it would be worth it to pay twice for

that phone (which is what the warranty costs) not to have to pay to replace >> it.

To which you were told that you were wrong, because you were shown that there's more valid reasons than only 'affordability'.

On Mon, 11 Aug 2025 14:20:11 -0400, -hh wrote :

To his point, I said in my *first* response that you insure that which you >>> can't afford to replace. If you're so destitute that you can't even afford >>> to replace your phone, then maybe it would be worth it to pay twice for

that phone (which is what the warranty costs) not to have to pay to replace >>> it.

To which you were told that you were wrong, because you were shown that

there's more valid reasons than only 'affordability'.

We agreed. I don't have to repeat *everything* that we already agreed on.

...

Facts are

that there's many different ways to calculate insurance rates and what you're trying to insinuate has very little bearing.

On Mon, 11 Aug 2025 19:33:40 -0400, -hh wrote :

Facts are

that there's many different ways to calculate insurance rates and what

you're trying to insinuate has very little bearing.

There is only one way to calculate true costs, and that's to add them up.

Take a look at the thread I referenced where AppleCare pushes up the cost

of the iPhone to the point that you pay double the original price.

Unless you trade that iPhone in after four years of paying for AppleCare.

Then you only paid 1-1/2 to 1-3/4 the price of the iPhone since you get

about 1/2 the price back on the original price paid for the iPhone.

It's why the most expensive phone to own is always going to be an iPhone.But the average product costs aren't irrelevant. Since iPhones trend to

There is only one way to calculate true costs, and that's to add them up.

Which only works in a deterministic world.

Unfortunately for you, insurance is stochastic.

Take a look at the thread I referenced where AppleCare pushes up the cost

of the iPhone to the point that you pay double the original price.

Irrelevant, for what matters are the rates of warranty claims, with

their respective costs. What the actual insured product happens to be (phone, car, house, person) doesn't change these business principles.

Unless you trade that iPhone in after four years of paying for AppleCare.

Then you only paid 1-1/2 to 1-3/4 the price of the iPhone since you get

about 1/2 the price back on the original price paid for the iPhone.

Since that's ignoring warranty claim rates & costs, that's grossly crude

& erroneous, which is why you came to invalid conclusions.

It's why the most expensive phone to own is always going to be an iPhone.But the average product costs aren't irrelevant. Since iPhones trend to

be more expensive, where did you appropriately & correctly normalize

this variable out? Because failure to do so is a rookie mistake.

On Tue, 12 Aug 2025 09:05:35 -0400, -hh wrote :

Anyway, you're correct ...

Where you're correct is that premium:claim ratios are not deterministic

when making estimates on whether or not the insurance will be worth it

simply because there is an unknown of whether or not bad things happen.

But wait....

There's a way around that randomness and uncertainty.

Which is how I calculated whether or not the insurance was worth it.

You assume an average of 2 events needing insurance, one big & one small.

In the four years, that's one event on average every two years.

Is it deterministic? Nope.

But it becomes strategically predictable.Because at best its a first order approach. It isn't sufficient for acompetitive business who wants to actually stay in business to use.

My calculations were not pure randomness; they were informed estimation.Numbers you made up because you lack stochastic data to do it correctly.

...Sure, the principles of risk pooling and pricing based on claim rates and costs are consistent across insurance types. But the nature of the insured product absolutely influences how those principles play out in practice.

A phone warranty deals with frequent, low-cost claims.

A house? Infrequent, high-cost, and often influenced by external

systemic risks like natural disasters or market shifts.

A person? Now you're in the realm of health,

mortality, and behavioral unpredictability.

So yes, the math behind insurance is universal, but the inputs,

assumptions, and volatility vary wildly depending on what's being insured.

That's not just a detail as it's the difference between modeling something

as simple as a cracked screen versus modeling an entire human life.

you've not been quantitatively honest on its value estimate.Unless you trade that iPhone in after four years of paying for AppleCare. >>>

Then you only paid 1-1/2 to 1-3/4 the price of the iPhone since you get

about 1/2 the price back on the original price paid for the iPhone.

Since that's ignoring warranty claim rates & costs, that's grossly crude

& erroneous, which is why you came to invalid conclusions.

Hmmm... now you're talking like an Apple troll since I took into account

the warranty claims. I assumed one major and one minor claim in 4 years.Keyword "assumed". Unless the policy is restricted to only two claims,

It's why the most expensive phone to own is always going to be an iPhone. >> But the average product costs aren't irrelevant. Since iPhones trend tobe more expensive, where did you appropriately & correctly normalize

this variable out? Because failure to do so is a rookie mistake.

Now you're talking back like a normal person and less like an Apple troll.

Sure, Android phones cost from free to just as much or more than iPhones. iPhones only cost in the high end, so we have to take that into account.

Most of the time the easiest way to take that into account is to compare similar phones, but since an iPhone will always lack functionality compared to Android, the big problem there is no similar phone can ever be found.

But at least we can compare similarly priced phones.

The overall cost of ownership of an iPhone is always going to be about

twice that of similarly priced Androids, and the iPhone functionality will

be about half (which is a known factor but harder to assess the value of).

Anyway, back to the original topic, if people want to pay an arm and a leg (plus huge deductibles) for a warranty that I got for free, all the powerOh, you actually know what Apple's net profit margin is for AppleCare?

to them, as it increases Apple's profits tremendously when they do so.

But I don't want to ever hear them claim Apple makes better product just because Apple has ungodly profits - as the reason those profits are high is that Apple marketing tells the Apple customer what to do & they just do it.Apple is able to have high margins because of successful marketplace differentiation of their products. Just what that differentiation is

On 8/12/25 13:27, Marion wrote:

On Tue, 12 Aug 2025 09:05:35 -0400, -hh wrote :

Anyway, you're correct ...

As per usual; "Film at 11".

Where you're correct is that premium:claim ratios are not deterministic

when making estimates on whether or not the insurance will be worth it

simply because there is an unknown of whether or not bad things happen.

But wait....

There's a way around that randomness and uncertainty.

Which is stochastic.

Which is how I calculated whether or not the insurance was worth it.

You assume an average of 2 events needing insurance, one big & one small.

In the four years, that's one event on average every two years.

Is it deterministic? Nope.

Incorrect: you're trying to use a deterministic method in the absence

of you having the stochastic data to do it correctly.

But it becomes strategically predictable.Because at best its a

first order approach. It isn't sufficient for a

competitive business who wants to actually stay in business to use.

My calculations were not pure randomness; they were informed estimation.Numbers you made up because you lack stochastic data to do it correctly.

...Sure, the principles of risk pooling and pricing based on claim rates and >> costs are consistent across insurance types. But the nature of the insured >> product absolutely influences how those principles play out in practice.

Which are manifest in claim rates & claim costs (one's stochastic data).

A phone warranty deals with frequent, low-cost claims.

Interesting claim ... but got substantiating data? Didn't think so.

A house? Infrequent, high-cost, and often influenced by external

systemic risks like natural disasters or market shifts.

Maybe. There's others which you're clearly unaware of.

A person? Now you're in the realm of health,

mortality, and behavioral unpredictability.

Maybe. There's others which you're clearly unaware of.

So yes, the math behind insurance is universal, but the inputs,

assumptions, and volatility vary wildly depending on what's being insured.

Nevertheless, they're all approached the same: stochastically.

That's not just a detail as it's the difference between modeling something >> as simple as a cracked screen versus modeling an entire human life.

A device dies; a person dies: is there really a difference?

you've not been quantitatively honest on its value estimate.Unless you trade that iPhone in after four years of paying for AppleCare. >>>>

Then you only paid 1-1/2 to 1-3/4 the price of the iPhone since you get >>>> about 1/2 the price back on the original price paid for the iPhone.

Since that's ignoring warranty claim rates & costs, that's grossly crude >>> & erroneous, which is why you came to invalid conclusions.

Hmmm... now you're talking like an Apple troll since I took into account

the warranty claims. I assumed one major and one minor claim in 4 years.Keyword "assumed". Unless the policy is restricted to only two claims,

It's why the most expensive phone to own is always going to be an iPhone. >>> But the average product costs aren't irrelevant. Since iPhones trend to >>> be more expensive, where did you appropriately & correctly normalizethis variable out? Because failure to do so is a rookie mistake.

Now you're talking back like a normal person and less like an Apple troll.

So did you normalize out this factor, or didn't you?

Sure, Android phones cost from free to just as much or more than iPhones.

iPhones only cost in the high end, so we have to take that into account.

So did you normalize out this factor, or didn't you?

Most of the time the easiest way to take that into account is to compare

similar phones, but since an iPhone will always lack functionality compared >> to Android, the big problem there is no similar phone can ever be found.

But at least we can compare similarly priced phones.

That requires modulation based on the respective service plans; did you?

The overall cost of ownership of an iPhone is always going to be about

twice that of similarly priced Androids, and the iPhone functionality will >> be about half (which is a known factor but harder to assess the value of).

Was TCO been normalized by lifespan? Because iPhones are known to last longer than Android on average; by some reports by 33%-66% longer for Samsung, and even longer for the Android off-brands:

<https://www.bankmycell.com/blog/average-lifespan-of-smartphone>

TL;DR: merely another variable required for an objective analysis.

Anyway, back to the original topic, if people want to pay an arm and a leg >> (plus huge deductibles) for a warranty that I got for free, all the powerOh, you actually know what Apple's net profit margin is for AppleCare?

to them, as it increases Apple's profits tremendously when they do so.

Please post what it is, along with substantiating citations (preferably

from their SEC filings, since it is perjury to be untruthful therein).

But I don't want to ever hear them claim Apple makes better product justApple is able to have high margins because of successful marketplace differentiation of their products.

because Apple has ungodly profits - as the reason those profits are high is >> that Apple marketing tells the Apple customer what to do & they just do it.

Just what that differentiation is

based on doesn't effectively matter, but because they've been successful over repeated purchase cycles, it is clear that their success isn't

merely marketing hype, but is substantiative for their customers.

BUT, this time I just took the iPhone over to the local Apple Store, confident that if it was the charging port it could be fixed or even replaced under AppleCare+ terms. It took about 5 minutes to repair. Accumulated lint in the port that the store rep cleaned out. If the

Apple rep had screwed up the port in the process so be it. The peace of

mind knowing I would not be buying another phone is worth the monthly premium to me.

On 8/11/2025 7:06 AM, Tom Elam wrote:

<snip>

BUT, this time I just took the iPhone over to the local Apple Store,

confident that if it was the charging port it could be fixed or even

replaced under AppleCare+ terms. It took about 5 minutes to repair.

Accumulated lint in the port that the store rep cleaned out. If the

Apple rep had screwed up the port in the process so be it. The peace

of mind knowing I would not be buying another phone is worth the

monthly premium to me.

Debris in the Lightning Port is a well known issue, probably the biggest "repair" other than batteries and screens. You can clean it out with a

can of compressed air, or a toothpick, no need for AppleCare+ for that.

On 2025-08-13 11:25, sms wrote:

On 8/11/2025 7:06 AM, Tom Elam wrote:

<snip>

BUT, this time I just took the iPhone over to the local Apple Store,

confident that if it was the charging port it could be fixed or even

replaced under AppleCare+ terms. It took about 5 minutes to repair.

Accumulated lint in the port that the store rep cleaned out. If the

Apple rep had screwed up the port in the process so be it. The peace

of mind knowing I would not be buying another phone is worth the

monthly premium to me.

Debris in the Lightning Port is a well known issue, probably the

biggest "repair" other than batteries and screens. You can clean it

out with a can of compressed air, or a toothpick, no need for

AppleCare+ for that.

I find G•U•M brand soft picks are great for cleaning out the port:

<https://i5.walmartimages.com/asr/d4ecd427-1965-48ab-b6f5-875bc2fddaaf.2d245a5673d4024b9cd62d35dc3c123f.jpeg>

Spiky rubber coating on the tip helps to grab onto the lint.

On 2025-08-13, Alan <nuh-uh@nope.com> wrote:

On 2025-08-13 11:25, sms wrote:

On 8/11/2025 7:06 AM, Tom Elam wrote:

<snip>

BUT, this time I just took the iPhone over to the local Apple Store,

confident that if it was the charging port it could be fixed or even

replaced under AppleCare+ terms. It took about 5 minutes to repair.

Accumulated lint in the port that the store rep cleaned out. If the

Apple rep had screwed up the port in the process so be it. The peace

of mind knowing I would not be buying another phone is worth the

monthly premium to me.

Debris in the Lightning Port is a well known issue, probably the

biggest "repair" other than batteries and screens. You can clean it

out with a can of compressed air, or a toothpick, no need for

AppleCare+ for that.

I find G•U•M brand soft picks are great for cleaning out the port:

<https://i5.walmartimages.com/asr/d4ecd427-1965-48ab-b6f5-875bc2fddaaf.2d245a5673d4024b9cd62d35dc3c123f.jpeg>

Spiky rubber coating on the tip helps to grab onto the lint.

I picked up one of these long ago and use it regularly. It's great:

<https://www.purplemohawk.biz>

On 8/11/25 21:40, Marion wrote:

On Mon, 11 Aug 2025 19:33:40 -0400, -hh wrote :

Facts are

that there's many different ways to calculate insurance rates and what

you're trying to insinuate has very little bearing.

There is only one way to calculate true costs, and that's to add them up.

Which only works in a deterministic world.

Unfortunately for you, insurance is stochastic.

-hh <recscuba_google@huntzinger.com> wrote:

On 8/11/25 21:40, Marion wrote:

On Mon, 11 Aug 2025 19:33:40 -0400, -hh wrote :Which only works in a deterministic world.

Facts are

that there's many different ways to calculate insurance rates and what >>>> you're trying to insinuate has very little bearing.

There is only one way to calculate true costs, and that's to add them up. >>

Unfortunately for you, insurance is stochastic.

I think you mean probabilistic. If it was truly random/stochastic actuaries would not be able to model risk and insurance would be the same for

everyone.

On Mon, 11 Aug 2025 19:33:40 -0400, -hh wrote :

Facts are

that there's many different ways to calculate insurance rates and what

you're trying to insinuate has very little bearing.

There is only one way to calculate true costs, and that's to add them up.

Take a look at the thread I referenced where AppleCare pushes up the cost

of the iPhone to the point that you pay double the original price.

Unless you trade that iPhone in after four years of paying for AppleCare.

Then you only paid 1-1/2 to 1-3/4 the price of the iPhone since you get

about 1/2 the price back on the original price paid for the iPhone.

It's why the most expensive phone to own is always going to be an iPhone.

It's why the most expensive phone to own is always going to be an iPhone.

At $120/year it's 8 years before the premiums = cost. That assumes no claims. If the phone breaks and is not repairable you get a new phone.

| Sysop: | DaiTengu |

|---|---|

| Location: | Appleton, WI |

| Users: | 1,064 |

| Nodes: | 10 (0 / 10) |

| Uptime: | 146:20:33 |

| Calls: | 13,691 |

| Calls today: | 1 |

| Files: | 186,935 |

| D/L today: |

22 files (1,452K bytes) |

| Messages: | 2,410,869 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}